Given the lack of a comprehensive guide on the home-buying process — with information scattered across Reddit and other platforms — I decided to write this article based on my own experience.

Keep in mind that buying a house is often a lengthy, time-consuming, and challenging process, especially in the Netherlands. Everyone's experience can vary. The points I discuss aren't definitive and may differ based on your circumstances, but they provide a solid overview of what to expect.

Prerequisites

At the outset, evaluate your financial situation. Can you cover the various costs associated with buying a house — fees for consultants, notaries, and other expenses? Beyond the mortgage itself, you'll need approximately €7,000 to €10,000 depending on your circumstances (I've detailed these costs at the end).

This amount covers incidental purchase costs and is separate from any overbid amount.

Permanent Contract

The most important factor in securing a mortgage is having a permanent contract. You either need a permanent employment contract, or a "Declaration of Intent" letter from your employer indicating they plan to renew your contract.

In the Netherlands, a permanent contract offers significant job security — the employer can rarely terminate it except under very special circumstances. Banks value this stability highly.

- A declaration of intent can reduce the loan amount, so a permanent contract is more advantageous.

- For couples, it's sufficient for one person to have a permanent contract. If both do, the loan amount increases accordingly.

Checking Your Loan Range

Dutch home mortgages typically span 30 years. To estimate your potential loan, use an online mortgage calculator — the ABN Bank calculator is one of the simplest and most reliable. Enter your details and get an approximate figure accurate to within 1–2%.

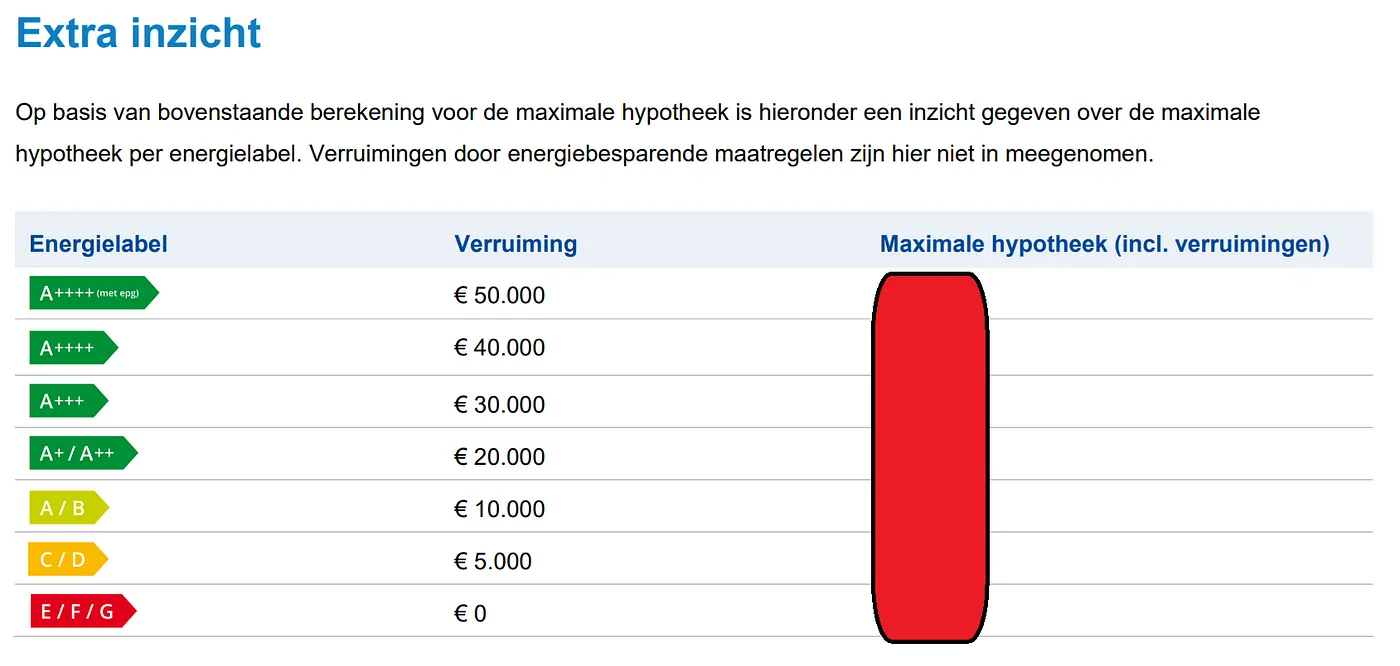

Your loan amount can also increase based on the energy label of the house, thanks to government subsidies for higher energy efficiency. For example, if your maximum loan is €500K and the house has an A+ label, your loan could increase to €520K.

Mortgage Advisor

A mortgage advisor guides you through the entire process — preparing documents, applying for a loan, securing the bank guarantee, and more. Since all documents are in Dutch, they handle correspondence on your behalf.

Having a mortgage advisor in the Netherlands is essential.

Bank-Affiliated vs. Independent

- Bank-affiliated advisors work for a specific bank. They'll help you secure a mortgage from that bank only.

- Independent advisors aren't tied to any single bank. They can shop around for better rates and terms.

The fee is legally regulated and fixed at roughly €2,500–€3,000 regardless of which type you choose.

I went with an independent advisor — and it paid off. The first bank they applied to denied our loan citing a three-year residency requirement I hadn't heard of. My advisor immediately applied to another bank, which approved without issue. That flexibility is the real advantage.

Initial Consultation

Most advisors offer one or two free initial sessions to assess your situation before you sign a contract. After that, they'll request documents including:

- Employer statement (contract type, income, holiday allowance)

- Latest payslip

- Passport and residence card

- UWV report (obtainable via DigiD)

- Declaration of debts and savings

Finding a House

The main platform is Funda — all properties eventually end up there. Buying here is fundamentally different from many other countries. Coming from Iran, I was used to visiting an agent, negotiating, and meeting somewhere in the middle. In the Netherlands, houses are publicly listed and go through a single-round sealed bid process. No back-and-forth negotiation.

Real Estate Agent (Makelaar)

A Makelaar accompanies you on viewings, inspects the property, and — crucially — determines the real market value of a house. This protects you from overbidding out of desperation.

A colleague was bidding on a house listed at €350K. His agent discovered a comparable property nearby had sold for €340K the month before. They underbid, and he bought it for €340K — below asking price.

Broker fees vary: some charge a fixed fee (~€4,000), others charge ~1% of the house price.

Should you hire one? If you're new to the Netherlands, don't speak Dutch fluently, and lack a local network — yes, seriously consider it. I've seen people spend months searching on their own without success. The agent's network and market knowledge can make the difference.

Finding a Broker

- Personal recommendations — most reliable

- Search on Funda — includes ratings and reviews

Broker contracts typically include 10–12 property visits. Beyond that, expect an extra €50–60 per visit.

Visiting a House

Before using one of your contracted broker visits, scout the area yourself first. Photos are staged to look their best — the neighborhood might not match your expectations. Save your visits for properties you're genuinely interested in.

On platforms like move.nl, you can request detailed property data: year of construction, materials, energy costs, heating systems, insulation, and more. Use this before committing to a viewing.

Bidding

Every house in the Netherlands must be publicly listed and sold through a single-round bid. When you visit, ask: "When is the bid day?" The agent will give you a deadline — e.g., "Monday at noon."

Your bid includes:

- Proposed price — what you're willing to pay

- Mortgage dependency — how much you're financing

- Personal savings — how much you're covering yourself

Example: "I want this house for €500K — €480K mortgage, €20K savings."

Listing Price vs. Actual Value

The listing price on Funda is typically set ~10% below actual market value to generate bidding competition. Don't treat it as the real price.

The home valuation price is what the bank's appraiser determines. The bank lends based on this number, not your bid. If you bid €480K but the bank values the house at €460K, they'll only lend €460K — the gap comes from your pocket.

Why Savings Matter

If you bid €480K relying entirely on a mortgage, and the bank only approves €470K, your bid looks risky to the seller. But if you have €15K in savings and bid €480K as €465K loan + €15K savings, the seller sees a more secure offer — even if the valuation comes in slightly lower than your bid.

If the valuation ends up higher than expected, you'll need less from savings. Small wins like this happen.

Bid Results

Results aren't communicated proactively — if you don't hear back, your bid wasn't selected. Once accepted, the house status on Funda changes to "Under offer."

After two consecutive rejections on different houses, our broker called with surprising news: we were second choice on both. The first bidders had their loans rejected, and the sellers turned to us. On the same day, we had offers accepted on two houses and got to choose which one we wanted. I think that's a Guinness record for the Netherlands. 😄

Technical Inspection

Optional, but recommended for older houses. A specialist inspects the property and provides a detailed report categorizing costs into:

- Short-term — immediate fixes (e.g., €1,400 for specific repairs)

- Mid-term — issues to address within a few years

- Improvement — optional upgrades

Use short-term costs to negotiate a price reduction or ask the seller to fix issues before closing.

Check especially for: foundation condition, moisture under the floor, pests in wooden structures, sewer system integrity.

Cost: ~€500.

Pre-Sale Agreement

Once both parties agree, an electronic pre-sale agreement is signed by buyer, seller, and both brokers. The house status changes to "Sold under reservation." The sale is pending mortgage approval and deposit payment.

Notary

The notary (arranged by the seller's agent) handles the final paperwork. They'll request documents from both parties and set three key dates:

- Withdrawal deadline — last date you can legally back out (e.g., if the loan is rejected)

- Bank guarantee deadline

- Notary date — when you sign in person, money is transferred, keys handed over

A translator in your native language is mandatory on notary day — the notary arranges this in advance.

Bank Guarantee

To reassure the seller you won't back out, you must deposit 10% of the purchase price with the notary — or provide a bank guarantee for the same amount.

If you don't have that liquidity (common), intermediary companies issue a bank guarantee for ~0.1% of the property price. For a €500K house, that's ~€500. Your mortgage advisor handles this.

Once the guarantee is in place, the sale is final. Neither party can back out.

Cost Summary

| Item | Required | Approximate Cost |

|---|---|---|

| Mortgage advisor | Yes | €2,500–€3,000 |

| Real estate agent (Makelaar) | No | ~1% of house price |

| Property valuation | Yes | ~€800 |

| Technical inspection | No | ~€500 |

| Land registry | Yes | €300–€500 |

| Bank guarantee | Yes | €300–€500 |

| Translator (notary day) | Yes | ~€400 |

| Transfer fee | Yes | €40–€100 |

| Incidental taxes | Yes | €100–€500 |

| Transfer tax (2%) | Yes* | Exempt if under 35 and house < €520K |

A Few Final Notes

You don't pay anyone anything until the notary date — except for the technical inspection and home valuation, which are paid immediately after the service. All other fees are settled at the end.

One useful tool: WOZ Waardeloket — enter any postal code to see the municipality's assessed value by year. It's a government site used for property tax estimates. Post-COVID price rises mean it often lags behind market reality, but it gives useful historical context.

Good luck. It's a process, but when you get those keys, it's worth it.